Analysis of the Systemic Impact of the Iran-Iraq Conflict on the Global shipping Industry

[kadence_subtitle]

The escalating tensions between Israel and Iran affects the global shipping industry chain deeply. Given our company’s focus on shipping – related products like ships, engines, spare parts, and more, this development is of particular significance. The far – reaching impacts span across multiple aspects such as maritime security, various ship types, order dynamics, ushering the industry into a new era of “dual – cycle growth in energy – focused shipping and military vessels.”

I. Soaring Maritime Security Risks and the Jeopardy of Key Shipping Lanes

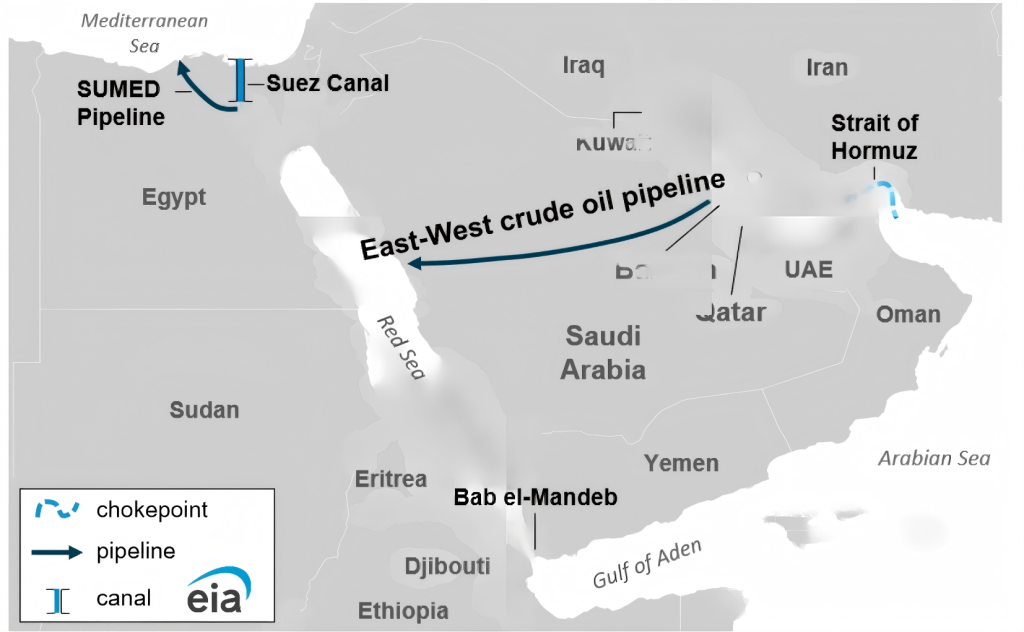

The Middle East stands as a linchpin in global maritime energy transportation, with the Strait of Hormuz being a critical chokepoint. Any exacerbation of the Iran – Israel conflict will make the navigational safety of this strait a pivotal factor in the global shipping market. Handling about 20% of the world’s crude oil seaborne trade and serving as a vital route for Qatar’s LNG exports, the Strait of Hormuz is of utmost importance. A worsening situation will compel ships to take detours, either off the Omani coast or via more circuitous routes. This not only hikes up the ton – mile requirements but also slashes ship turnaround efficiency, leading to a temporary shortfall in shipping capacity. Additionally, war – risk premiums and surcharges will skyrocket. Historically, during times of Middle East unrest, the daily charter rates of VLCC tankers have seen exponential growth. For ships operating in these waters, the need for reliable spare parts becomes even more crucial to handle any potential damage or breakdowns during these challenging voyages.

II. Divergent Trends in Segmented Ship Markets

1. Tanker Market: Riding the Cyclical Wave of Benefits

Energy transportation is acutely sensitive to conflict – induced disruptions. Should the Middle East’s energy supply chain be disrupted, Europe and Asia will turn to alternative crude oil sources like the US and Brazil. This shift will substantially lengthen the shipping distances, thereby fueling the demand for VLCCs and Suezmax tankers. As a result, freight rates will strengthen in a cyclical manner, enhancing the profitability of shipowners. These tankers rely on a complex network of engines and various spare parts to function optimally, and with increased demand and longer voyages, the need for quality spare parts for engines and other components will be on the rise

2. LNG Carrier Market: Bolstering Strategic Demand

Amid the backdrop of Europe’s energy restructuring efforts, any disruption to Middle Eastern LNG supplies will trigger a rapid reconfiguration of the global LNG trade. With increased LNG exports from the US and other regions, the demand for LNG carriers will soar, keeping high – end ship industry capacity in short supply. LNG carriers are highly specialized ships, and the engines and their associated spare parts need to meet stringent safety and performance standards to ensure the safe transportation of liquefied natural gas.

3. Container Ship Market: Encountering Short – Term Headwinds

The decline in throughput at Middle Eastern ports and the necessity of rerouting are taking a toll on container liner on – time performance. This has introduced greater uncertainty in voyages, negatively impacting container shipping efficiency and escalating costs in the short term. Container ships, like other vessels, require regular maintenance and replacement of spare parts, and the current situation may pose challenges in ensuring timely availability of these parts due to disruptions in supply chains.

4. Auxiliary Vessel Market: Embracing Structural Expansion

The intensifying conflict has spurred regional countries to boost their naval budgets, leading to a surge in demand for auxiliary vessels, including frigates, patrol ships, replenishment ships, oil replenishment vessels, and unmanned surface vessels (USVs). Concurrently, this is driving up the demand for medium – speed diesel engine power systems. Auxiliary vessels play a crucial role in naval operations and maritime support, and their engines and spare parts need to be robust and reliable to withstand various operational conditions.

III. The Shift in ship industry Order Structures

1. Surge in Military and Quasi – Military Orders

Under the shadow of security threats, regional countries are ramping up the expansion of their naval and coast guard fleets. This has led to an increased share of orders for military and quasi – military vessels. Shipyards and countries with expertise in constructing auxiliary vessels, along with those that can supply high – quality engines and spare parts for these vessels, are set to reap the benefits.

2. Divergence in Merchant Ship Orders

The order prospects for different merchant ship types are showing distinct structural variations:

| Ship Type | Impact Direction |

| Tankers | Significantly Beneficial |

| LNG Carriers | Beneficial |

| Container Ships | Short – Term Pressure |

| Dry Bulk Carriers | Neutral |

| Auxiliary Vessels | Strongly Beneficial |

IV. The Climb in Insurance, Financing, and Operating Expenses

In the context of war or conflict, ship operations are burdened with higher risk premiums. The cost of war – risk insurance is escalating, along with surcharges for high – risk sea areas. Moreover, the detours taken by ships to avoid danger zones are driving up fuel consumption and time – related costs. These increased costs will be transferred to freight rates, thereby extending the profit – making cycle of the shipping industry. For shipowners, this means that the cost of maintaining their ships, including the procurement of spare parts, may also increase due to the overall rise in operational expenses.

V. The Reshaping of Port Landscapes and Regional Shipping Hubs

If the tensions in the Persian Gulf persist, some shipping activities will gravitate towards relatively safer transshipment ports in Oman and the UAE, elevating their strategic significance. Additionally, ports in the Eastern Mediterranean may emerge as crucial nodes for energy transshipment and replenishment, thus redrawing the regional shipping map. These port changes can also impact the availability and distribution of ship spare parts, as shipping routes and supply chain networks are adjusted.

VI. Opportunities in the Marine Power and Equipment Industry Chain

In a conflict – ridden environment, the emphasis on ship safety and reliability has reached new heights. Military auxiliary vessels and oil tankers will experience a growing demand for medium – speed diesel engines. There will also be an increased focus on emergency power generation systems and redundant power configurations, along with a spike in demand for high – reliability equipment such as explosion – proof and shock – resistant components. This presents a golden opportunity for manufacturers of marine engines, related equipment, and spare parts to expand their market reach.

VII. Long – Term Ramifications: Industry Restructuring

Should the Iran – Israel conflict endure, the industry will undergo a series of structural realignments. Energy transportation routes will diversify, risk – mitigation measures such as detours will become standard practice, the demand for strategic reserve oil tankers will grow, and the need for military – civilian integrated vessels will continue to rise. The global shipping market will gradually transition from being solely trade – driven to a model propelled by “energy security + geopolitical security.”

Conclusion: The impact of the Iran – Israel conflict on the shipping industry is characterized by a distinct structural pattern. Tankers, LNG carriers, auxiliary military vessels, and marine propulsion systems, along with their associated spare parts, stand to gain significantly. Dry bulk shipping remains relatively unscathed, while container shipping and Middle Eastern ports face short – term setbacks. As the situation evolves, our company, with its focus on ships, engines, and spare parts, needs to closely monitor these trends to capitalize on emerging opportunities and navigate potential challenges in the global shipping market.