Chinese Natural Gas Power Generation and Distributed Energy : Current Status, Challenges, and Prospects

[kadence_subtitle]

The Chinese natural gas power generation (hereinafter referred to as “gas – fired power”) and distributed natural gas energy industries have traversed over a decade of development, yielding certain achievements. However, deep – rooted contradictions and development bottlenecks persist. This article delves into the industry’s development trajectory, analyzes the restrictive factors, and offers a forward – looking perspective, all based on the actual industry situation in 2026.

Development Journey: Progress Amidst Twists and Turns

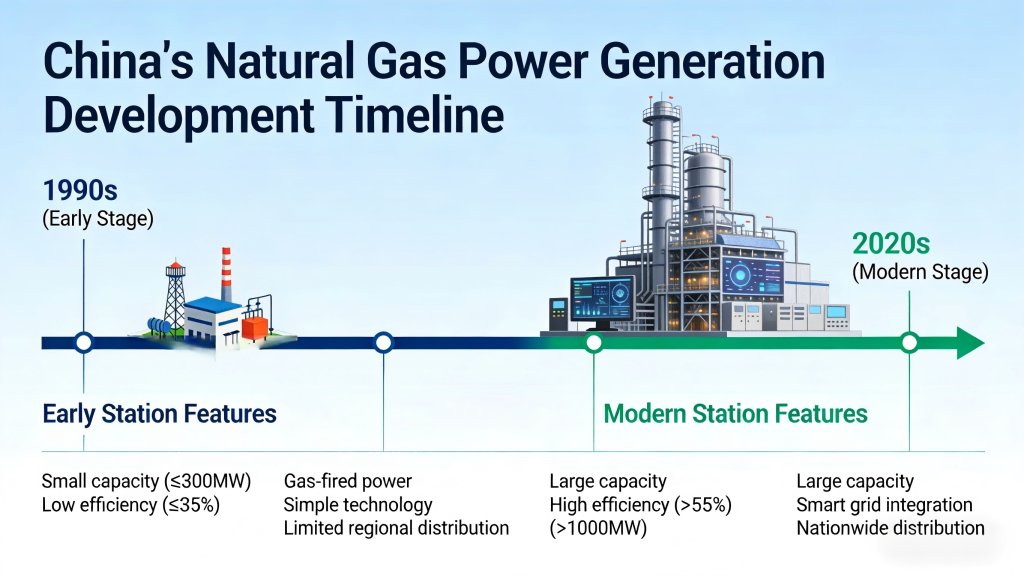

Four Phases of Gas – fired Power Development

1.Sporadic Growth Phase (-2003)

From the 1990s to 2003, coastal regions in China grappled with severe power shortages. In response, gas – fired power plants were erected in provinces like Guangdong and Zhejiang to provide emergency power supply. At this stage, the technology was relatively backward, and the efficiency was low. The installed capacity of gas – fired power accounted for less than 0.5% of the total national installed capacity.

2.Bundled – Bidding and Robust Development Phase (2003 – 2014)

Initiated in 2003, the bundled bidding for gas turbines, complemented by the launch of the West – East Gas Pipeline project, propelled the nation to place greater emphasis on gas turbine development. International heavyweights in the gas – turbine industry rushed to capture a share of the Chinese market. Unfortunately, the “market – for – technology” strategy failed to materialize, as core technologies remained firmly in the hands of foreign companies. By the end of 2014, the installed capacity of gas – fired power accounted for merely 4.2% of the total, and its peak – shaving potential had yet to be fully realized.

3.Overcapacity and Initial Technological Breakthrough Phase (2014 – 2020)

The acquisition of Ansaldo by Shanghai Electric in 2014 disrupted the market equilibrium, intensifying competition within the industry. This led to a decline in prices, compelling companies to accelerate technological iteration. Domestic enterprises, in turn, ramped up their research and development efforts. As a result, the installed capacity of gas – fired power grew steadily, and its role in peak – shaving and emergency response began to gain wider recognition.

4.Self – improvement and Pressured – progress Phase (2021 – 2026)

During this period, there has been an acceleration in technological self – reliance. The dependence on imported core components has decreased significantly. The market positioning of gas – fired power has become more distinct, emerging as a crucial peak – shaving power source for renewable energy. As of the first half of 2026, the installed capacity has continued to climb, reaching 5.3% of the national total.

Six Phases of Natural Gas Distributed Energy Development

1.Spontaneous Exploration Phase (-2011)

After the establishment of the first distributed energy station in 1998, the industry embarked on a journey of spontaneous exploration. Projects were predominantly concentrated in large – scale public buildings and industrial parks, resulting in a limited development scale.

2.Policy – driven Promotion Phase (2011 – 2013)

In 2011, multiple government departments jointly issued guiding opinions, which spurred rapid growth in projects. Nevertheless, due to the lack of adequate policy support, the project implementation rate remained disappointingly low.

3.Stagnation Phase (2013 – 2015)

The upward trend of natural gas prices during this period dealt a heavy blow to both new and existing projects, causing the development of the distributed energy industry to come to a standstill.

4.Rapid Development Phase (2015 – 2017)

A significant reduction in gas prices in 2015 ignited investment enthusiasm. However, the gas shortage at the end of 2017 dealt a setback to project development.

5.Hesitation, Downturn, and Rational Re – evaluation Phase (2018 – 2020)

In the aftermath of the gas shortage, investment became more cautious, and the industry entered a downturn. Investors began to place greater emphasis on project economics and gas supply stability. A “city – gas – dominated” pattern emerged, but the industry’s development remained sluggish.

6.Policy – enhancement and Difficulty – alleviation Phase (2021 – 2026)

Under the “dual – carbon” target, increased policy support has expanded the application scenarios of distributed energy. Nevertheless, challenges such as profitability and grid – connection issues still loom large. By the first half of 2026, the installed capacity has doubled, yet it still falls short of the planned target.

Development Hurdles: A Multitude of Constraints

Electricity Pricing and Profitability Quandaries

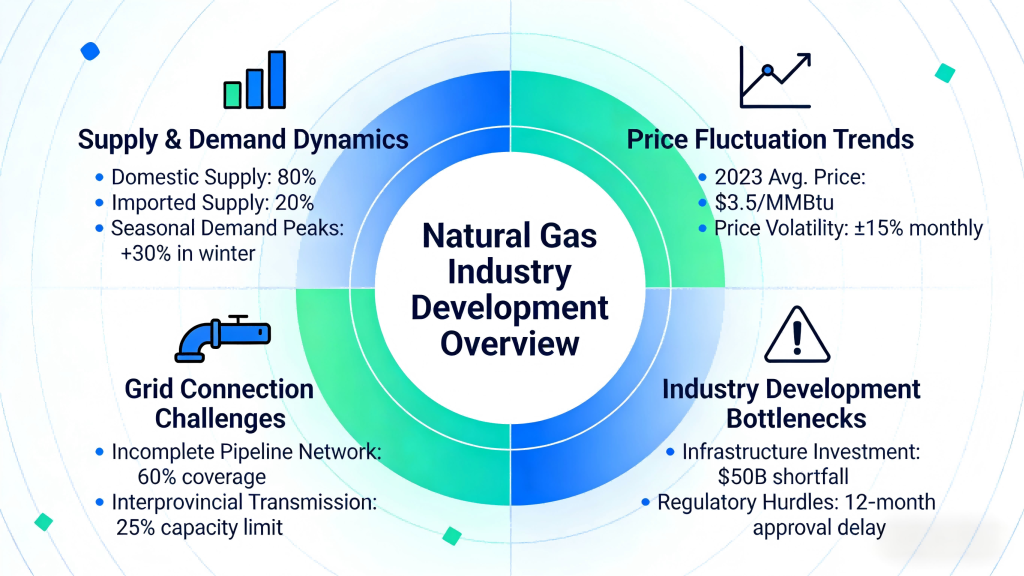

Although there have been optimizations in gas – fired power subsidies, a fully – fledged market – based pricing mechanism is yet to be established. Gas – fired power faces the conundrum of high costs and low selling prices. Insufficient compensation for ancillary services, coupled with the withdrawal of provincial – level subsidies, has significantly exacerbated the profit – making pressure on enterprises. For distributed energy, the ambiguity of grid – connection price standards has made it arduous for “surplus electricity to be fed into the grid,” severely weakening its profitability.

Natural Gas Supply – demand Imbalances

Despite an improvement in natural gas supply capacity, high – volatility prices and seasonal supply shortages remain persistent issues. Gas – fired power, being a major gas – consuming sector, is constantly exposed to supply risks. The incomplete market – based pricing reform further complicates the situation, as it becomes difficult to transfer cost increases. Moreover, distributed energy projects often suffer from weak gas – supply security.

Distributed Grid – connection and Business Model Impediments

Although the grid – connection process for distributed energy has been streamlined, practical implementation still encounters numerous obstacles. The “power – sales – beyond – the – wall” model has not been fully rolled out. Business models are overly simplistic, technological levels require substantial improvement, and there is a conspicuous shortage of operation and management talent.

Technological and Competitive Challenges

Notable breakthroughs have been achieved in the localization of gas – fired power technology. However, a significant reliance on imported core components persists, and operation and maintenance technology lags behind international standards. The core equipment for distributed energy also presents challenges. Simultaneously, the market is witnessing intensifying competition, with wind power and solar power emerging as formidable competitors.

Development Prospects: Opportunities and Challenges Coexist

Opportunities:

1. Policy Support: Under the “dual – carbon” goal, the strategic significance of natural gas has been elevated. Future policies are anticipated to refine electricity pricing mechanisms, increase compensation for ancillary services, and introduce other supportive measures.

2. Market Demand: With economic development fueling electricity demand, gas – fired power is witnessing a growing demand in eastern regions as a peak – shaving and emergency power source. The application scenarios for distributed energy are also expanding, opening up new market frontiers.

3. Technological Breakthroughs: The accelerated localization of gas – fired power and distributed energy technologies is expected to reduce costs and enhance project profitability.

4. Ample Gas Supply: Factors such as the commissioning of global LNG projects are likely to lead to an ample gas supply and stable gas prices, thereby improving the economic viability of related projects.

Challenges: Constraints related to electricity pricing mechanisms, natural gas prices, distributed grid – connection, and technological localization remain largely unaddressed.